The Section 25D Residential Clean Energy Credit, which covered 30% of residential solar installation costs, expired on December 31, 2025. The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, eliminated this credit with no phase-down period and no extension. Homeowners who completed installations by the deadline can still claim the credit on their 2025 tax returns, but systems placed in service on or after January 1, 2026 receive no direct federal tax benefit.

For solar installers and contractors navigating the solar permitting process, this policy shift changes how projects are structured, financed, and sold. The good news is that residential solar remains a strong investment in 2026. Third-party ownership (TPO) arrangements still qualify for the Section 48E commercial tax credit through December 31, 2027, state incentives continue to reduce costs in many markets, and rising utility rates are shortening payback periods even without federal support. This guide covers every available pathway for homeowners going solar in 2026 and explains what each option means for your project timeline, AHJ permitting requirements, and overall return on investment.

What Happened to the Section 25D Solar Tax Credit?

Section 25D of the Internal Revenue Code authorized a tax credit equal to 30% of qualified residential clean energy property costs. The OBBBA (H.R. 1) amended this section to terminate the credit for expenditures made after December 31, 2025. Under IRS guidance, an “expenditure” is treated as made when original installation is completed, not when a contract is signed or a deposit is paid. This means the physical installation must have been finished and the system operational by year-end 2025 to qualify.

The Inflation Reduction Act of 2022 had previously extended the 30% credit through 2032, followed by a step-down to 26% in 2033 and 22% in 2034. The OBBBA accelerated this timeline by approximately nine years, eliminating the credit entirely rather than phasing it down. Unlike previous extensions and modifications of Section 25D, there was no transition period for projects already in progress.

| Time Period | Credit Rate (Under IRA) | Credit Rate (Under OBBBA) | Status |

| 2022 through 2025 | 30% | 30% | Available (systems placed in service by Dec 31, 2025) |

| 2026 | 30% | 0% | Eliminated – no credit for owned systems |

| 2027 through 2032 | 30% | 0% | Eliminated |

| 2033 | 26% | 0% | Eliminated |

| 2034 | 22% | 0% | Eliminated |

Key Deadlines Homeowners Need to Know

Several critical dates determine which federal incentives remain available and how homeowners can access them. Solar installers and solar engineering teams should keep these deadlines in mind when advising clients and planning project schedules.

| Deadline | What It Affects | Action Required |

| December 31, 2025 | Section 25D (homeowner-owned systems) | System must have been installed and operational by this date to claim the 30% credit |

| April 15, 2026 | 2025 tax return filing | File IRS Form 5695 to claim the credit for qualifying 2025 installations |

| July 4, 2026 | Section 48E safe harbor | TPO projects must begin construction by this date to preserve the four-year completion window |

| December 31, 2027 | Section 48E placed-in-service deadline | TPO solar projects not safe-harbored by July 4, 2026 must be fully installed by this date |

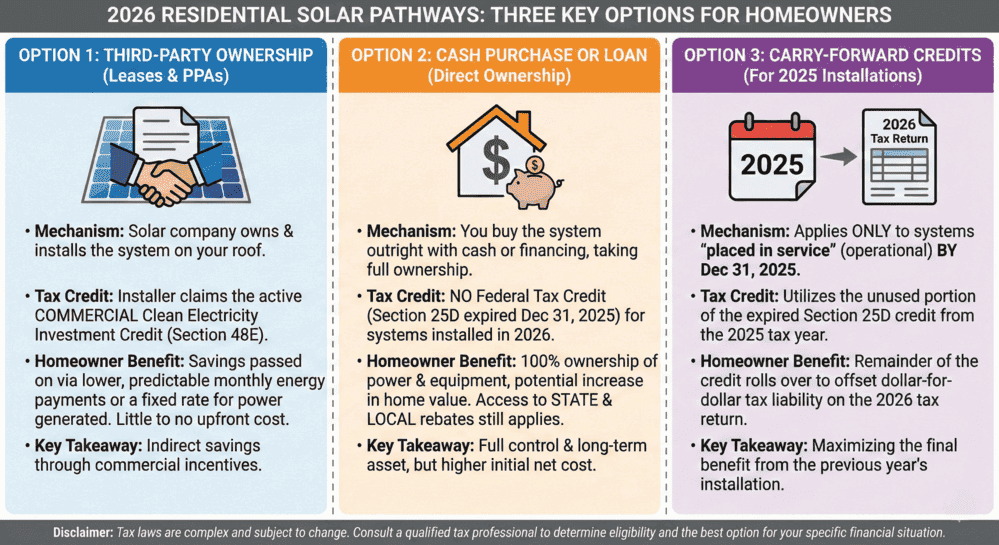

Option 1: Third-Party Ownership Through Leases and PPAs

The most significant pathway to federal tax credit savings in 2026 runs through third-party ownership. Solar leases and power purchase agreements (PPAs) qualify for the Section 48E Clean Electricity Investment Tax Credit, which provides a 30% credit to the business entity that owns the system. The business then passes a portion of that savings to the homeowner through lower monthly payments or reduced per-kilowatt-hour rates.

Under a solar lease, the homeowner pays a fixed monthly amount to use the equipment. Under a PPA, the homeowner pays only for the electricity the system produces, typically at a rate lower than the local utility. In both cases, the TPO provider handles system maintenance, monitoring, and warranty claims. Homeowners benefit from lower energy costs without the responsibility of system ownership during the initial agreement period.

How TPO Economics Work in 2026

When a TPO provider installs a system on a homeowner’s roof, the provider claims the Section 48E credit on their federal tax return. For a system costing $25,000, the provider receives a $7,500 credit (30% base rate). If the project qualifies for the 10% Domestic Content Bonus Credit and is located in an Energy Community, the provider can claim up to $12,500 in combined credits. These savings are factored into the homeowner’s pricing, which is why TPO arrangements often deliver immediate bill savings with $0 down.

FEOC Compliance Requirements

Starting in 2026, all projects claiming the Section 48E credit must comply with Foreign Entity of Concern (FEOC) restrictions. At least 40% of the value of all manufactured products in the solar system must come from manufacturers that are not affiliated with prohibited foreign entities, including companies based in or controlled by China, Russia, Iran, or North Korea. This threshold increases by 5% annually, reaching 60% by 2030. For battery storage, the initial threshold is 55% in 2026, increasing to 75% by 2030.

These restrictions directly affect which equipment TPO providers can install. Homeowners entering lease or PPA agreements in 2026 should expect a more limited selection of panels, inverters, and batteries compared to previous years. TPO providers maintain approved vendor lists (AVLs) that only include FEOC-compliant equipment, and these lists are updated regularly as manufacturers certify their supply chains.

Prepaid Solar Leases and PPAs

A growing option in 2026 is the prepaid solar lease or PPA. In this arrangement, the homeowner makes a single upfront payment, typically around 70% of what a cash purchase would cost, to cover 20 to 25 years of solar energy. The TPO provider owns the system during the first six years (the tax credit recapture period), claims the Section 48E credit, and passes the savings through as the upfront discount. After the recapture period, most contracts include a $0 or nominal-fee buyout option, giving the homeowner full ownership.

Prepaid arrangements combine many advantages of both ownership and leasing. The homeowner locks in low-cost energy for the full agreement term with no monthly payments, and the upfront cost is 20% to 30% lower than a direct purchase because the provider monetizes the tax credit. This structure is particularly attractive in states where utility interconnection policies and net billing rates make long-term ownership valuable.

| Feature | Cash Purchase | Solar Loan | Solar Lease | Solar PPA | Prepaid Lease/PPA |

| Federal tax credit | None (25D expired) | None (25D expired) | 48E (claimed by provider) | 48E (claimed by provider) | 48E (claimed by provider) |

| System ownership | Homeowner from day one | Homeowner from day one | Provider (20-25 years) | Provider (20-25 years) | Provider (6 years), then homeowner |

| Upfront cost | $18,000 to $30,000 | $0 down | $0 down | $0 down | 70% of purchase price |

| Monthly payments | None | Loan payment | Fixed monthly lease | Per-kWh rate | None after upfront payment |

| Maintenance responsibility | Homeowner | Homeowner | Provider | Provider | Provider (then homeowner) |

| Equipment selection | Unrestricted | Unrestricted | FEOC-compliant AVL only | FEOC-compliant AVL only | FEOC-compliant AVL only |

| 25-year savings potential | Highest | High (minus interest) | Moderate | Moderate | High |

Solar Permit Solutions

Homeowner Going Solar?

Get the permit-ready plan set your city requires — delivered fast so your solar project stays on schedule.

Option 2: Cash Purchase or Loan Without the Federal Credit

Buying a solar system outright or financing with a loan remains a viable option in 2026, even without the 30% federal credit. Direct ownership delivers the highest long-term savings because the homeowner captures 100% of the energy production value over the system’s 25 to 30-year lifespan. The trade-off is a higher effective upfront cost and a longer payback period compared to pre-2026 installations.

According to EIA Electric Power Monthly data, average U.S. residential electricity rates have increased at an annual rate exceeding inflation since 2022. In high-cost markets like California, the Northeast, and parts of the Southwest, electricity costs are projected to continue rising, which strengthens the financial case for solar even without federal incentives. The typical payback period for a purchased system in 2026 falls in the 8 to 12-year range nationally, though homes in high-rate territories with favorable net metering can see payback as short as 5 to 7 years.

How the Numbers Work Without Section 25D

Consider a 7 kW system installed in 2026 at a cost of $22,000. Without the 30% credit, the homeowner pays the full amount. If the system offsets $2,200 in annual electricity costs and the homeowner’s utility rate increases 4% annually, the simple payback period is approximately 10 years. After payback, the system generates roughly $55,000 to $72,000 in cumulative electricity savings over its remaining 15 to 20-year lifespan. That represents a return of 250% to 327% on the original investment.

By comparison, the same system installed in 2025 with the 30% credit would have cost the homeowner $15,400 after the $6,600 credit, resulting in a 7-year payback. The difference is meaningful, but the underlying economics of solar, producing electricity for less than the utility charges, have not changed. For homeowners with NEC-compliant installations on suitable rooftops, the investment still outperforms most alternatives over a 25-year horizon.

Solar Loan Considerations in 2026

Before 2026, many solar loans were structured around the assumption that the homeowner would use their tax credit refund to make a lump-sum principal reduction in year one. These “dealer fee” loan products offered lower initial monthly payments with the expectation that the balance would drop significantly after the credit was claimed. Without the Section 25D credit, this loan structure no longer works for new installations.

In 2026, homeowners financing with loans should look for products with straightforward terms: fixed interest rates, no dealer fees, and payment amounts that reflect the full system cost from day one. Credit unions, home equity lines of credit (HELOCs), and property-assessed clean energy (PACE) financing are alternatives that may offer competitive rates without relying on tax credit assumptions.

Option 3: Carry-Forward Credits for 2025 Installations

Homeowners who completed their solar installation in 2025 but whose tax liability was too low to claim the full 30% credit in a single year can carry forward the unused portion to future tax years. The IRS has confirmed that the carry-forward provision remains in effect and has not announced an expiration date for unused credit.

For example, a homeowner who installed a $25,000 system in 2025 would be eligible for a $7,500 credit. If their 2025 federal tax liability is only $3,000, they claim $3,000 on their 2025 return and carry the remaining $4,500 forward. That $4,500 can offset tax liability in 2026, 2027, or subsequent years until fully used. Because the system was placed in service in 2025, the 2025 rules apply, and the credit does not expire simply because Section 25D was terminated for new installations.

The IRS requires homeowners to file IRS Form 5695 (Residential Energy Credits) with their tax return to claim the credit. Tax professionals should note that while Form 5695 will continue to be used for carry-forward claims, the form may be revised in future years since no new Section 25D credits will be generated.

State and Local Incentives That Remain in 2026

With the federal residential credit gone, state and local programs become the primary mechanism for reducing solar costs for homeowners who choose direct ownership. The Database of State Incentives for Renewables and Efficiency (DSIRE) catalogs available programs by state. Here are the most significant state-level incentives that remain available in 2026.

| State | Incentive | Value | Notes |

| New York | NY-Sun + State Tax Credit | 25% of cost, up to $5,000 | Among the strongest state-level substitutes for the federal credit |

| South Carolina | State Solar Energy Tax Credit | 25% of cost | Unused credit carries forward for 10 years |

| Massachusetts | SMART Program + State Tax Credit | 15% credit (up to $1,000) + production-based payments | Battery adders increase value significantly |

| Arizona | Residential Solar Energy Tax Credit | 25% of cost, up to $1,000 | No expiration date; 5-year carry-forward |

| New Jersey | Successor Solar Incentive (SuSI) | Performance-based SREC payments | Among the most valuable production incentives nationally |

| Illinois | Adjustable Block Program | Lump-sum SREC payments | Available for systems up to 25 kW |

| California | SGIP (battery storage) | Varies by utility territory | Property tax exclusion expires January 1, 2027 |

| Multiple states | Sales and property tax exemptions | Varies | Over 25 states exempt solar from sales tax and/or property tax increases |

For solar contractors handling residential solar permit requirements across multiple states, understanding which state incentives are available helps position projects correctly. In states like New York and South Carolina, the state tax credit can replace a substantial portion of the lost federal benefit. In states without meaningful state incentives, TPO arrangements become the default recommendation for cost-conscious homeowners.

How Utility Rate Trends Support Solar in 2026

The financial case for solar has always been driven more by utility rate avoidance than by tax incentives. EIA data shows that average residential electricity prices have increased roughly 25% since 2020, with some states experiencing even steeper hikes. In 2025 alone, states including New Jersey, Pennsylvania, and Florida saw rate increases ranging from 10% to 20%.

This trend directly benefits solar economics. Every dollar increase in annual electricity costs shortens the payback period for a solar installation. For a homeowner paying $0.25 per kWh today, even a modest 3% annual increase means their rate reaches approximately $0.45 per kWh in 20 years. A solar system that locks in electricity production at an effective cost of $0.07 to $0.10 per kWh becomes increasingly valuable each year as the spread between solar and utility costs widens.

The OBBBA itself may contribute to higher electricity costs in the near term. The legislation includes provisions that expand fossil fuel production and reduce clean energy deployment incentives, which could shift the national generation mix in ways that increase wholesale electricity prices. For homeowners weighing the solar decision in 2026, the question is not whether utility rates will rise, but how quickly.

Battery Storage: Essential for Maximizing 2026 Solar Value

Without the Section 25D credit, battery storage becomes even more important for optimizing solar ROI. Batteries allow homeowners to store excess solar production during midday hours and discharge it during expensive peak-rate periods, significantly increasing self-consumption and reducing grid dependence.

Under time-of-use (TOU) rate structures, which are standard in states like California, Arizona, and parts of the Northeast, batteries can reduce payback periods from 12 to 15 years (solar-only) to 7 to 9 years (solar plus storage). The value comes from peak shaving, where stored solar energy displaces the most expensive utility kWh rather than being exported at low net billing rates.

For homeowners pursuing TPO arrangements, battery storage can often be included in the lease or PPA. The TPO provider claims the Section 48E credit on the battery as well, further reducing the homeowner’s effective cost. Standalone battery systems under third-party ownership continue to qualify for tax credits through 2032, making this a particularly durable incentive pathway.

Solar contractors should factor battery storage into every solar permit design conversation in 2026. The combination of declining battery costs, rising TOU rate differentials, and grid reliability concerns makes storage a compelling addition regardless of the federal tax credit landscape.

Permitting and Interconnection Implications

The Section 25D expiration does not change any solar permitting requirements. Building permits, electrical permits, structural reviews, and utility interconnection applications remain identical whether the system is owned by the homeowner or a TPO provider. However, the shift toward TPO financing creates several practical differences in the permitting workflow.

TPO providers typically have established relationships with permitting offices and utilities, which can accelerate approvals. They also maintain standardized design templates that meet NEC 690 requirements and local AHJ specifications. For installers transitioning more of their business to TPO models, working with a solar permit design service ensures that plan sets meet both the AHJ’s structural and electrical requirements and the TPO provider’s documentation standards.

Interconnection timelines remain the same regardless of ownership structure. Utilities like APS in Arizona, Con Edison in New York, and PG&E in California process residential interconnection applications on the same timeline whether the system is homeowner-owned or leased. The key difference is that TPO providers generally include interconnection management in their service, whereas homeowner-purchased systems may require the installer to manage this process independently. For projects in states with streamlined online permitting, tools like DOE solar resources can help homeowners understand what to expect at each stage.

What Solar Installers Should Tell Homeowners

The end of Section 25D requires a fundamental shift in how solar professionals present the value proposition. Instead of leading with “save 30% with the federal tax credit,” the conversation should center on long-term electricity cost avoidance, energy independence, and the specific financial structure that best fits the homeowner’s situation.

According to data from SEIA and NREL, installed solar costs have declined approximately 70% over the past decade. Even without the federal credit, the levelized cost of solar electricity from a residential system is substantially below retail utility rates in most U.S. markets. The credit was never the reason solar worked financially. It was an accelerator that shortened payback periods and improved near-term returns.

For contractors handling commercial and residential solar permitting, offering both owned and TPO options gives homeowners a clear choice. In many cases, the optimal recommendation depends on the homeowner’s tax situation, their planned length of homeownership, the local utility’s net billing or net metering policy, and which state incentives are available.

Conclusion: Solar Remains a Strong Investment in 2026

The expiration of Section 25D removes one tool from the residential solar toolkit, but it does not fundamentally change the economics that make solar a sound investment. Utility rates continue rising, installed system costs continue declining, and battery storage technology continues improving. For homeowners who preferred direct ownership, the investment still delivers strong returns over the system’s lifespan, even if the payback period is 3 to 5 years longer than it would have been with the credit.

For homeowners who want to access federal incentives, TPO arrangements through leases, PPAs, and prepaid products provide a clear path through at least December 31, 2027. These structures are well-established, widely available, and in many cases deliver immediate monthly savings with no upfront cost. The Section 48E credit ensures that the federal government continues supporting residential solar adoption, just through a different mechanism than the one homeowners were accustomed to.

Solar installers, contractors, and solar permit design professionals should prepare for a market where TPO products become the dominant sales channel and where state incentives carry more weight in the financial conversation. Understanding the full range of available options, from cash purchase to prepaid PPA, positions your business to serve every homeowner regardless of their financial situation or tax profile. Contact Solar Permit Solutions for expert permit design and engineering support that keeps your projects moving through this transition.

Frequently Asked Questions

Can homeowners still get a federal solar tax credit in 2026?

Homeowners cannot claim the Section 25D credit for systems installed in 2026 or later. However, homeowners can still benefit from the Section 48E commercial tax credit indirectly through third-party ownership arrangements such as solar leases, PPAs, and prepaid solar products. In these arrangements, the TPO provider claims the 30% credit and passes savings to the homeowner through lower pricing. This pathway remains available through December 31, 2027.

What is the solar payback period without the federal tax credit?

The typical payback period for a purchased solar system in 2026 ranges from 8 to 12 years nationally, compared to 5 to 8 years when the 30% credit was available. However, payback varies significantly by location. Homes in high-cost electricity markets with favorable net metering, such as California, New York, New Jersey, and Massachusetts, can still achieve payback periods of 5 to 7 years. States with low utility rates and no local incentives may see payback periods of 12 to 15 years.

Can I carry forward unused Section 25D credit from my 2025 installation?

Yes. If your system was installed and operational by December 31, 2025, and your tax liability was insufficient to claim the full 30% credit, the IRS allows you to carry forward the unused portion to future tax years. The OBBBA did not change the carry-forward rule. Any excess credit from your 2025 return can offset future tax liability in 2026, 2027, and beyond. The IRS has not announced an expiration date for carrying forward unused Section 25D credit.

What are FEOC requirements and how do they affect residential solar in 2026?

Foreign Entity of Concern (FEOC) restrictions apply to projects claiming the Section 48E commercial tax credit, which includes all TPO residential solar installations (leases, PPAs, and prepaid products). Starting in 2026, at least 40% of the value of manufactured products in the system must come from non-FEOC manufacturers. This threshold rises to 45% in 2027 and continues increasing annually. FEOC restrictions do not apply to homeowner-owned systems purchased with cash or loans, since those systems are not claiming any federal tax credit in 2026.

Is solar still worth it in 2026 without the tax credit?

Yes. Solar remains a strong investment in 2026 for most U.S. homeowners. The primary financial driver is utility rate avoidance, not tax credits. Average residential electricity rates have increased roughly 25% since 2020 and continue to trend upward. A solar system that produces electricity at an effective cost of $0.07 to $0.10 per kWh delivers significant savings against utility rates of $0.15 to $0.40 per kWh depending on location. Over a 25-year system lifespan, cumulative savings typically range from $40,000 to $100,000, producing returns of 200% to 400% on the original investment even without any federal credit.

What is the difference between a solar lease and a solar PPA in 2026?

A solar lease requires a fixed monthly payment to rent the equipment regardless of production. A PPA charges the homeowner a set per-kilowatt-hour rate for the electricity the system produces, so payments vary with actual output. Both qualify for the Section 48E tax credit through the TPO provider. PPAs tend to align costs more closely with actual energy production, while leases provide more predictable monthly bills. In 2026, both options typically offer immediate Day 1 savings compared to the homeowner’s utility bill, with no upfront cost.

Does the Section 25D expiration affect solar permitting requirements?

No. Building permits, electrical permits, structural reviews, and utility interconnection requirements are identical regardless of whether a system is homeowner-owned or leased. The permitting process is governed by local AHJ rules and NEC code requirements, not federal tax policy. The only practical difference is that TPO providers often include permitting and interconnection management as part of their service, which can streamline the process for homeowners.

When does the Section 48E commercial solar tax credit expire?

The Section 48E credit for wind and solar projects placed in service after December 31, 2027 is only available if construction began on or before July 4, 2026. Projects that begin construction by that safe harbor date have up to four years to complete installation. Projects that miss the July 4, 2026 construction start deadline must be fully placed in service by December 31, 2027. Energy storage technology is not subject to the accelerated wind and solar termination and follows the standard Section 48E timeline.

Homeowner Going Solar?

Get the permit-ready plan set your city requires — delivered fast so your solar project stays on schedule.

SPS Editorial Team

Solar Permit Solutions

Solar Permit Solutions provides professional solar permit design services for residential, commercial, and off-grid installations across all 50 states. Our team ensures permit-ready plan sets delivered fast.

Related Articles

Utility Interconnection Requirements for Solar Installers: The 6 Rules Every Utility Enforces

interconnection agreement, UL 1741 and IEEE 1547 certified inverters, a utility-...

How to Respond to Solar Permit Corrections (And Get Approved on Resubmission)

To respond to a solar permit correction, read every comment from every reviewing...

Can an EV Charging Station Be Powered by Solar? Here’s How to Build One

Yes, an EV charging station can be powered by solar. A grid-tied solar array pai...